Bitcoin, Tokenized Gold, and The Race For The Digital Store-of-Value Premium

Two distinct frameworks are currently competing for the same monetary premium in digital asset markets. One is a fixed-supply cryptographic protocol with sixteen years of price history and a $1.33 trillion market capitalization. The other is physical gold, an asset with a $36 trillion market cap and a five-thousand-year monetary track record, increasingly accessible via blockchain infrastructure. How those frameworks perform relative to each other over the next decade will shape the architecture of institutional digital asset allocation in ways that are only beginning to be priced.

This analysis examines the empirical case for each asset’s claim to the “digital store of value” designation, the market data bearing on that claim through Q1 2026, and the structural conditions under which each scenario; Bitcoin absorbing gold’s monetary premium, or tokenized gold absorbing Bitcoin’s, becomes more or less probable.

The data does not resolve the question cleanly. Both assets hold defensible positions within distinct monetary frameworks. What the data does reveal is a meaningful divergence between the narrative supporting Bitcoin’s store-of-value thesis and the behavioral evidence accumulating against it, alongside an accelerating set of onchain gold metrics that most institutional analysis has not yet incorporated into its framing.

Framing the Monetary Competition

Bitcoin’s store-of-value thesis rests on four properties its architects designed explicitly to mirror gold: fixed terminal supply (21 million coins), predictable issuance declining on a known schedule, a cost-of-production floor via proof-of-work mining, and sovereign resistance by design. Satoshi Nakamoto’s 2008 whitepaper drew the analogy directly, and it has defined Bitcoin’s institutional positioning ever since. The “digital gold” narrative was not a marketing afterthought. It was the structural thesis from which most major institutional allocation argument derived.

That thesis has been consequential. Between 2020 and 2024, it carried Bitcoin from a $200 billion to a $2 trillion asset class. Paul Tudor Jones, citing monetary debasement risk, allocated to it publicly in 2020. MicroStrategy redenominated its corporate treasury in Bitcoin on an explicit store-of-value rationale. BlackRock’s January 2024 spot ETF application cited Bitcoin’s “unique investability” as a scarce, non-sovereign asset. The institutional architecture built around this framing is now substantial.

Tokenized gold represents a structurally different proposition. Products such as Tether Gold (XAUT) and Pax Gold (PAXG) issue blockchain tokens backed one-to-one by allocated physical gold held in audited, insured vaults. The token carries no speculative premium and makes no claim to superior monetary properties — it is simply gold, settled on distributed ledger infrastructure. The monetary credentials it carries are those of the underlying commodity, earned across every major fiat currency collapse, sovereign debt crisis, and inflationary episode in recorded economic history.

The question this analysis addresses is whether these two frameworks are genuinely competing for the same capital, and if so, what the current data suggests about trajectory.

Tokenized Gold: Market Data Through Q1 2026

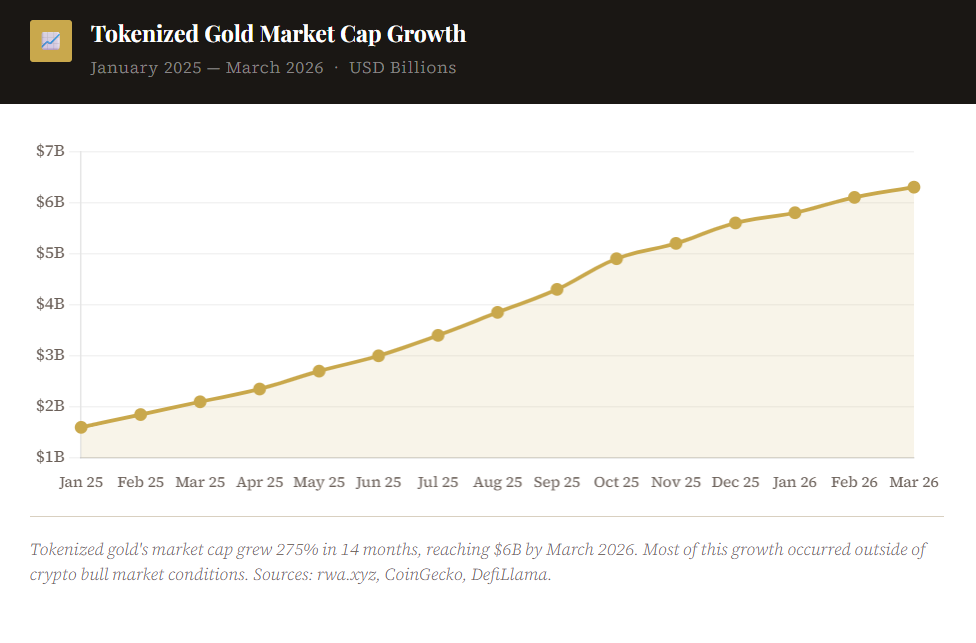

The tokenized gold market has expanded significantly faster than most institutional observers anticipated. Market capitalization grew from approximately $1.6 billion in January 2025 to over $6 billion by March 2026, a 275% increase over fourteen months. In 2025 alone, market cap growth reached 177%. Trading volume over the same period grew 1,550%, a rate approximately ten times that of the largest traditional gold ETFs over the equivalent period.

To contextualize the volume figures: tokenized gold’s cumulative trading volume in 2025 reached $178 billion, surpassing every US-listed gold ETF except the SPDR Gold Shares (GLD). The number of distinct token holders grew by over 115,000 during the year, a rate fourteen times higher than the prior year. Monthly transfer volume recorded a 63% increase within a single month in Q4 2025. As of March 2026, the tokenized commodities market overall has crossed $7.3 billion in market capitalization, with gold-backed tokens comprising the dominant share.

Critically, this growth did not occur during a favourable period for crypto markets broadly. Bitcoin and the wider digital asset market experienced significant drawdowns across much of 2025. The tokenized gold expansion appears to have been driven by distinct demand — institutional interest in onchain gold infrastructure and, as discussed below, capital rotation out of more volatile digital assets during stress periods.

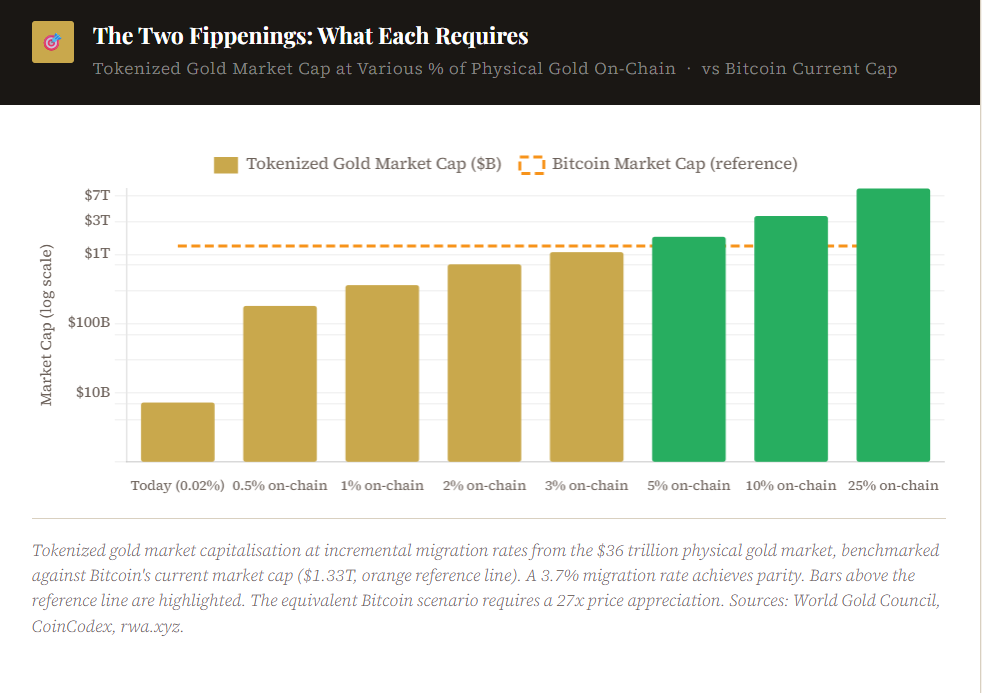

For comparative context, Bitcoin’s current market capitalization stands at approximately $1.33 trillion. Physical gold’s total market capitalization is estimated at approximately $36 trillion by the World Gold Council. A Bitcoin price of approximately $1.4 million per coin would be required for Bitcoin’s market cap to achieve parity with physical gold — a 25x appreciation from current levels. Tokenized gold, by contrast, represents less than 0.02% of the physical gold market by capitalization, and its path to scale is denominated in migration of existing assets rather than price appreciation of a new one.

The asymmetry in what each asset requires to close the gap with the other is a central input to the scenario analysis below. Bitcoin’s path to matching gold’s market cap is denominated in price appreciation of a volatile asset across a 27x multiple. Tokenized gold’s path to matching Bitcoin’s market cap is denominated in the percentage of existing physical gold that migrates to onchain infrastructure, a process driven by institutional convenience rather than speculative demand.

Bitcoin’s Correlation Profile: The Empirical Record

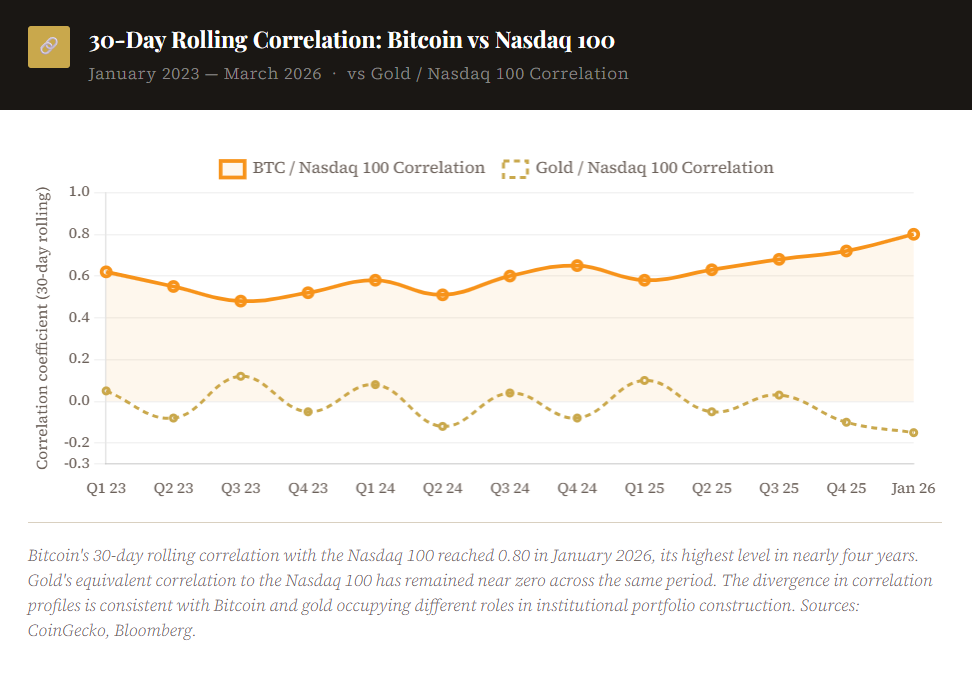

The theoretical case for Bitcoin as a store of value rests substantially on its expected behaviour during periods of macroeconomic stress. Specifically, its anticipated low or negative correlation with risk assets under conditions of market dislocation, mirroring the behaviour gold has demonstrated consistently across multiple crisis regimes. The empirical record through Q1 2026 does not support that expectation.

Gold’s correlation to risk assets during systemic stress has been extensively documented across twentieth-century monetary history. Its 30-day rolling correlation to major equity indices during the 2008 financial crisis, the 2011 European sovereign debt crisis, the 2020 COVID liquidity shock, and the 2022 rate-shock drawdown remained near zero or negative in each instance. Central banks hold gold as a reserve asset precisely because of this property, its monetary value derives from its demonstrated tendency to hold or appreciate purchasing power when other asset classes are contracting.

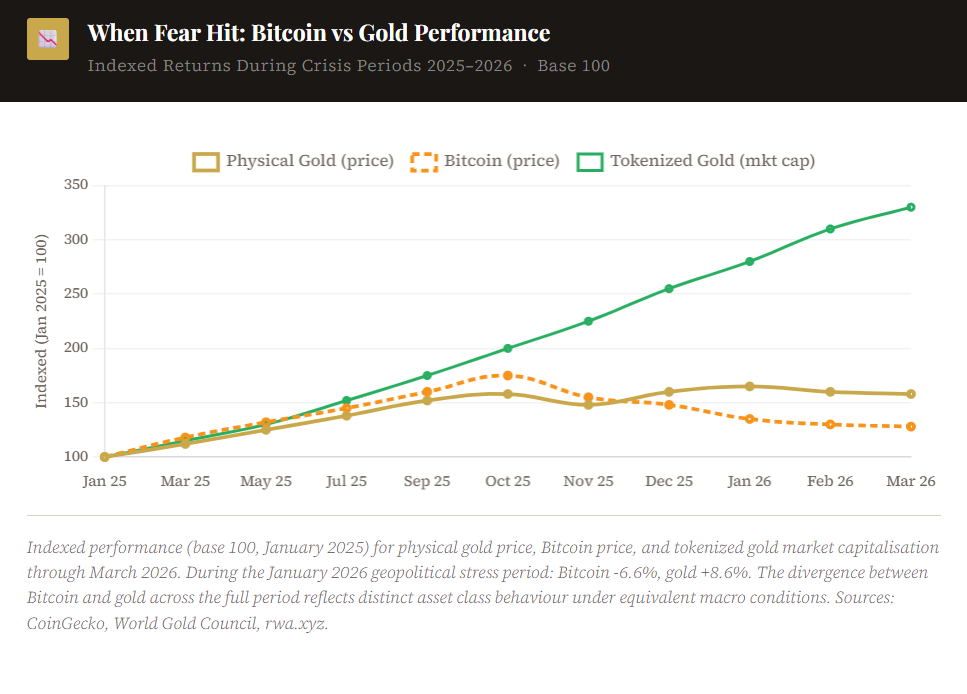

Bitcoin’s correlation profile has exhibited a different pattern. During the January 2026 period of elevated geopolitical stress, driven by US tariff escalation and regional military instability, Bitcoin declined 6.6% while gold appreciated 8.6% across the same window. The 30-day rolling correlation between Bitcoin and the Nasdaq 100 reached 0.80 during this period, its highest recorded level in nearly four years. A correlation coefficient of 0.80 to a technology-weighted equity index is characteristic of a high-beta growth asset, not a monetary reserve.

Over the full 2025 period, gold appreciated over 60%, reaching record levels above $5,000 per ounce. Bitcoin declined approximately 38% from its October 2025 peak, spending most of the year in a consolidation range. The two assets, which a significant share of institutional commentary had positioned as convergent stores of value, exhibited sharply divergent behaviour when the macro conditions most favourable to store-of-value assets materialised. In October 2025, during a significant Bitcoin liquidation event, tokenized gold daily trading volume increased 250% in a single session, suggesting active rotation from Bitcoin volatility into on-chain gold exposure.

Scenario Analysis: Two Paths to Market Cap Convergence

The term “flippening” in crypto markets conventionally refers to the hypothetical moment at which Ethereum’s market capitalization surpasses Bitcoin’s, a scenario that has been modelled extensively but has not yet occurred. A structurally distinct version of the same question is now relevant: under what conditions does tokenized gold’s market capitalization approach or exceed Bitcoin’s, and how does that probability compare to the inverse — Bitcoin achieving market cap parity with physical gold?

Both scenarios are analytically tractable. Both carry significant uncertainties. The inputs differ substantially in character.

Scenario A : Bitcoin Achieves Market Cap Parity with Physical Gold

Required condition: Bitcoin appreciates from its current price of approximately $63,000 to approximately $1.4 million per coin, producing a market capitalisation of roughly $36 trillion. This represents a 27x multiple from current levels.

The bull case for this scenario is substantive and should be engaged seriously. Bitcoin has historically produced returns of this magnitude across multiple market cycles. Its network effect, measured by onchain activity, developer ecosystem, institutional custody infrastructure, and regulatory recognition has compounded steadily for sixteen years. The approval of spot Bitcoin ETFs in multiple jurisdictions represents a structural shift in its accessibility to institutional capital. Corporate treasury adoption, led by MicroStrategy’s now substantial Bitcoin position, has created a new category of long-duration buyer. And a US administration that has publicly signalled pro-crypto regulatory positioning creates a materially different operating environment than any prior cycle.

Longer-term structural arguments also hold weight. If the dollar’s reserve currency status continues to erode, a trajectory consistent with current central bank diversification trends, a non-sovereign, algorithmically scarce digital asset becomes a more compelling reserve allocation. WisdomTree’s bull-case model, which requires Bitcoin above $110,000 as an entry condition, projects a path to gold parity under conditions of sustained global monetary expansion. That condition is not implausible given current fiscal trajectories in major economies.

The scenario’s key constraint is time and consistency of behaviour. A 27x appreciation in a volatile asset, while historically precedented in Bitcoin’s cycle history, requires sustained institutional confidence across multiple years without a disqualifying correlation event, specifically, a scenario in which Bitcoin declines significantly during a period of major macroeconomic stress. Each such event narrows the addressable market of investors willing to classify Bitcoin as a monetary reserve rather than a risk asset.

Scenario B : Tokenized Gold Achieves Market Cap Parity with Bitcoin

Required condition: A sufficient percentage of the $36 trillion physical gold market migrates to on-chain tokenized infrastructure to reach a market capitalisation of $1.33 trillion. The required migration rate is approximately 3.7% of physical gold outstanding.

Tokenized gold represents less than 0.02% of physical gold by market capitalization as of March 2026. The gap between current state and the required state is large. However, the nature of the required change differs structurally from Scenario A. This scenario does not require price appreciation of a volatile asset. It requires a shift in custody and settlement infrastructure preferences among holders of an existing $36 trillion asset class.

The infrastructure enabling this migration is already operational. Tether Gold and Pax Gold collectively custody over 1.2 million ounces of physical gold. The EU’s MiCA regulatory framework, which came into full effect in late 2024, mandates 1:1 physical backing and independent auditing for tokenized commodity products, addressing the counterparty risk concerns that have historically slowed institutional adoption. JPMorgan, BlackRock, and Morgan Stanley have each identified real-world asset tokenization as a priority use case in their digital asset infrastructure buildouts. McKinsey’s 2024 analysis projects the broader tokenized asset market reaching $2 trillion by 2030.

The institutional incentive structure is straightforward. An institution currently holding gold via a custodian or ETF gains 24/7 liquidity, near-instant settlement, programmable collateral functionality, and reduced custody friction by migrating to tokenized infrastructure. The underlying asset does not change. The incremental return on the migration decision is positive at scale, with the primary friction being operational inertia and regulatory comfort, both of which are declining as the infrastructure matures.

The scenario’s key constraint is that tokenized gold has not yet been tested as a monetary instrument during a major global liquidity crisis. Its track record, while promising on growth metrics, is short. The physical gold it represents carries five thousand years of monetary precedent; the tokenized wrapper carries approximately five years. Whether institutional counterparty risk concerns — however mitigated by auditing and regulatory frameworks, would suppress demand during a genuine systemic stress event remains an open empirical question.

The tokenized gold market grew at 2.6 times the rate of physical gold in 2025. That differential growth rate, sustained over a multi-year horizon, compresses the timeline for Scenario B materially. The variables most likely to accelerate it are regulatory clarity in major jurisdictions, continued buildout of DeFi collateral infrastructure that accepts tokenized gold, and sustained Bitcoin correlation to risk assets that reduces its attractiveness as a store-of-value allocation relative to a physically backed alternative.

The variable most likely to accelerate Scenario A is a major macroeconomic regime shift, specifically, a sustained dollar debasement event of sufficient magnitude to drive institutional reallocation toward non-sovereign monetary assets at scale. In that environment, both Bitcoin and tokenized gold would likely appreciate, though their relative performance would depend critically on how each asset’s correlation profile evolved under genuine monetary stress.

The Bitcoin Bull Case: Structural Arguments That Remain Intact

A balanced assessment requires explicit engagement with the arguments most often advanced by long-term Bitcoin advocates. Arguments that the correlation data and tokenized gold growth metrics do not fully invalidate.

First, Bitcoin’s network effect is structurally distinct from any prior digital asset. The combination of mining infrastructure, custody infrastructure, regulatory recognition, and institutional allocation machinery built around Bitcoin over sixteen years represents a form of path dependence that has not historically been unwound. Network effects in monetary assets tend to be durable. The dollar’s reserve currency status has persisted for decades beyond the conditions that originally created it.

Second, Bitcoin’s fixed supply is genuinely different in kind from gold’s supply dynamics. Gold supply grows approximately 1.5% per year through mining. Bitcoin’s effective supply growth is declining and will approach zero. Under a scenario of sustained monetary expansion and central bank balance sheet growth, this property becomes more rather than less relevant to reserve asset allocation.

Third, the correlation critique, while empirically grounded, is not necessarily permanent. Bitcoin’s correlation to risk assets has varied significantly across its history and may reflect its current market structure, dominated by retail and institutional investors with short time horizons rather than any intrinsic property of the asset. A sufficiently large and long-duration institutional holder base could, in theory, alter its correlation profile over time.

Fourth, Bitcoin has survived regulatory hostility, exchange collapses, mining bans, protocol forks, and multiple drawdowns exceeding 80% without a fundamental impairment to its network. That resilience is itself a form of track record that is relevant to reserve asset evaluation, even if it differs from gold’s track record in character.

These arguments do not resolve the correlation question. They do suggest that the question is not closed, and that a portfolio framework that excludes Bitcoin entirely on the basis of its current correlation profile may be underweighting its longer-term optionality.

Comparative Assessment

The table below summarizes the key attributes of each asset across dimensions relevant to monetary reserve and store-of-value assessment. The framing is descriptive rather than prescriptive, the relative weighting of these attributes will differ across investor mandates, time horizons, and risk frameworks.

When an institutional allocator evaluates both instruments against the properties conventionally associated with monetary reserves, the profile of each asset reflects a different set of trade-offs rather than a clear dominance of one over the other.

Outlook and Key Variables to Monitor

The balance of current evidence suggests a meaningful tension between the narrative framing that has driven Bitcoin’s institutional positioning and the behavioural data that has accumulated through Q1 2026. That tension does not resolve cleanly in either direction, and investors with different time horizons, risk tolerances, and monetary frameworks will weight the evidence differently.

Several variables will be most informative in determining which scenario gains trajectory over the next 24 to 36 months.

Bitcoin’s correlation profile under the next major stress event. If a significant macroeconomic dislocation occurs, such as a sovereign debt crisis, a major currency devaluation, or a sustained equity bear market, Bitcoin’s behaviour relative to gold will provide the most direct evidence on whether its correlation to risk assets is structural or cyclical. A decorrelation from equities under genuine stress would materially strengthen the store-of-value thesis. A continued high correlation would narrow the addressable institutional market for that narrative.

Tokenized gold adoption velocity among institutional custodians. The current growth rate of tokenized gold has been driven primarily by retail and smaller institutional demand. The more consequential shift would be adoption by sovereign wealth funds, pension funds, and central bank-affiliated entities as a complement or replacement for ETF-based gold exposure. Public signals of intent from major custodians in this direction would accelerate the Scenario B timeline considerably.

Regulatory treatment of tokenized commodities in the US. MiCA has established a framework in Europe. The equivalent US regulatory determination — whether tokenized gold is treated as a commodity, a security, or a distinct category, will significantly affect the speed of institutional adoption in the world’s largest asset management market.

The real-world asset tokenization buildout by major financial institutions. JPMorgan’s Onyx platform, BlackRock’s BUIDL fund, and similar institutional infrastructure projects are creating the plumbing through which tokenized gold would scale to institutional size. The pace of that buildout, and whether gold becomes a primary use case within it, will be a leading indicator of Scenario B’s trajectory.

Both assets are operating at the frontier of a genuine structural shift in how monetary value is stored and transferred digitally. The data through Q1 2026 indicates that tokenized gold is growing faster, correlating more reliably with its underlying monetary function, and attracting capital during Bitcoin stress events. It also indicates that Bitcoin retains a substantial network advantage, a deepening institutional infrastructure, and structural supply properties that no tokenized commodity can replicate.

The competition for the digital store-of-value premium is active, the outcome is not determined, and the variables that will resolve it are measurable. That makes it worth watching carefully.

Data sources: rwa.xyz, CoinGecko, DefiLlama (tokenized gold market capitalisation and volume, March 2026). CoinCodex and World Gold Council (Bitcoin and physical gold market capitalisation). McKinsey Global Institute (real-world asset tokenization market projections, 2024). WisdomTree Digital Assets research. Bloomberg (correlation data). All forward-looking statements represent scenario analysis and do not constitute investment advice. Past performance of any asset class referenced is not indicative of future results.